The 2026 regulatory landscape for cross-border trade

By 2026, the regulatory environment for B2B cross-border payments has shifted from voluntary best practices to mandatory, high-stakes compliance. Organizations handling international transactions must now navigate a complex web of legal requirements driven by Anti-Money Laundering (AML) and Know Your Customer (KYC) mandates. These regulations are no longer suggestions; they are legal necessities enforced by strict audit gates in the EU, US, and other major global jurisdictions.

In the European Union, the Markets in Crypto-Assets (MiCA) regulation and the upcoming Payment Services Directive 3 (PSD3) are reshaping how digital assets and traditional payments are monitored. These frameworks require financial institutions and payment service providers to implement robust verification procedures and real-time monitoring systems. The goal is to prevent illicit finance and ensure transparency in every cross-border transaction.

Similarly, in the United States, federal agencies continue to tighten enforcement of AML laws. The requirement for extensive verification procedures means that B2B entities must maintain multiple approval layers to prevent fraud and money laundering. This multi-layered approach is designed to protect the integrity of the global financial system while facilitating legitimate trade.

For global commerce, this means that compliance is no longer a back-office function but a core operational requirement. Companies must integrate these regulatory demands into their payment workflows, ensuring that every transaction is verified and reported according to the specific rules of the involved jurisdictions. Failure to adapt to these 2026 standards can result in severe penalties, frozen assets, and loss of banking relationships.

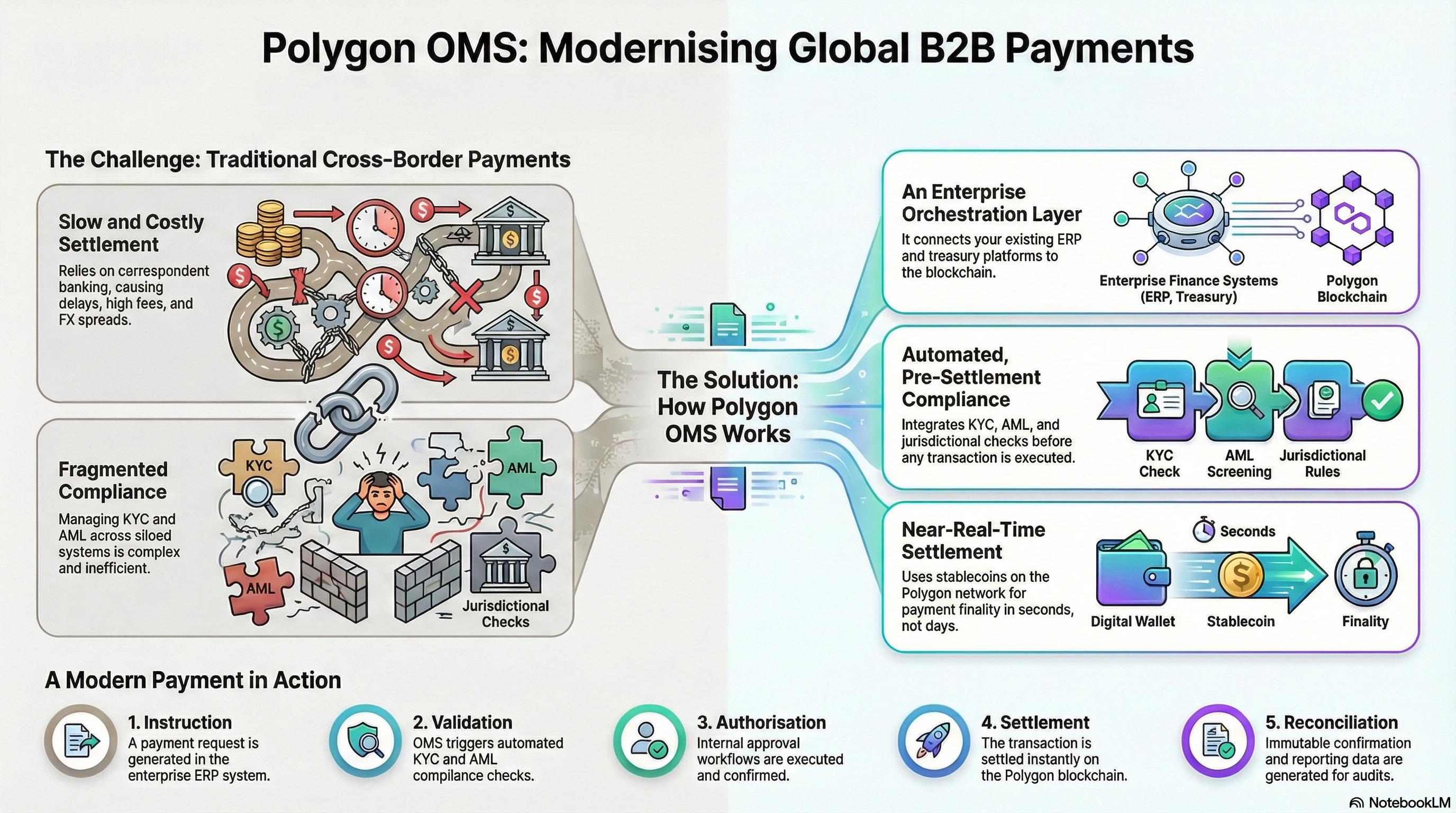

Stablecoins solve currency risk and speed settlement

B2B invoicing faces two mechanical friction points: foreign exchange (FX) volatility and settlement lag. Traditional cross-border payments rely on correspondent banking networks, which introduce multiple intermediaries. Each intermediary adds a layer of cost, opacity, and delay. In 2026, stablecoins offer a direct alternative by tokenizing value on distributed ledgers. This architecture allows businesses to settle invoices in minutes rather than days, while maintaining value stability through fiat-pegged mechanisms.

Eliminating FX volatility

Currency fluctuation creates uncertainty in B2B contracts. A purchase order agreed upon in January may lose value by the time it settles in March. Stablecoins mitigate this by providing a stable unit of account. For example, a US-based supplier can invoice a European buyer in a USD-pegged stablecoin. The buyer converts Euros to the stablecoin, and the supplier receives USD-equivalent value immediately. This eliminates the need for complex hedging instruments or forward contracts for routine transactions. The European Central Bank and US regulatory bodies monitor these mechanisms to ensure compliance with anti-money laundering (AML) standards.

Reducing settlement times

The traditional SWIFT network typically takes three to five business days to settle cross-border payments. Each day adds opportunity cost and working capital strain. Stablecoin settlements occur on-chain, often within seconds or minutes. This speed transforms cash flow management. Businesses can reinvest working capital faster, reducing the need for large cash reserves. According to Paystand’s 2026 B2B payment trends report, real-time settlement is a primary driver for adopting blockchain-based payment rails. This shift is particularly significant for global supply chains where timing is critical.

Compliance and audit trails

Regulatory scrutiny in 2026 requires robust audit trails for all financial transactions. Stablecoin transactions are recorded on immutable ledgers, providing transparent proof of payment. This visibility helps businesses comply with reporting requirements in the EU, US, and other jurisdictions. However, compliance also depends on the stablecoin issuer’s adherence to reserve requirements and KYC protocols. Businesses must verify that their payment partners use regulated issuers to avoid regulatory risk.

Practical implications for CFOs

For CFOs, the adoption of stablecoins means reevaluating treasury management strategies. The speed and stability of stablecoin settlements reduce the cost of capital and improve liquidity. However, integration requires technical infrastructure and staff training. Businesses should start with pilot programs for high-volume, low-margin transactions to test efficiency gains. As regulatory frameworks evolve, stablecoins may become a standard tool for B2B payment compliance.

ai invoice automation reduces disputes and errors

By 2026, the integration of artificial intelligence into accounts payable and receivable workflows has become a standard requirement for maintaining audit compliance. AI-driven invoice generation and matching systems process data with a precision that manual entry cannot match, significantly reducing the error rates that historically plagued B2B reconciliation. These systems automatically extract line items, tax codes, and purchase order numbers, cross-referencing them against contract terms and delivery receipts in real time.

The reduction in human error directly correlates to fewer payment disputes. When invoices are generated with consistent formatting and accurate data fields, the likelihood of mismatches during the three-way match process diminishes. This automation ensures that finance teams in the EU, US, and other major jurisdictions can demonstrate clear, auditable trails of invoice validation, satisfying regulatory requirements for financial transparency. According to industry analyses from TreviPay and OroInc, AI adoption in accounts receivable is a primary driver for operational efficiency and dispute reduction in 2026.

Smoother reconciliation allows finance departments to focus on exception management rather than routine data entry. By automating the validation of standard transactions, organizations can quickly identify and resolve anomalies, preventing delays in payment cycles. This shift not only accelerates cash flow but also strengthens vendor relationships by ensuring that payments are processed accurately and promptly, based on verified contractual obligations.

Compliance checks built into the payment rail

Modern B2B payment platforms are shifting from reactive monitoring to proactive enforcement by embedding compliance protocols directly into the transaction rail. In 2026, regulatory frameworks in the EU, US, and global markets require that verification steps occur automatically before funds settle. This structural integration ensures that B2B payment compliance 2026 standards are met without manual intervention, reducing operational friction and audit exposure.

KYC and AML checks are now triggered at the point of initiation. As noted by UATP in their 2026 industry analysis, multiple approval layers are designed to prevent illicit activity before it reaches the ledger. Platforms verify counterparty identity and transaction purpose in real-time, flagging discrepancies instantly. This approach aligns with the European Union’s revised Anti-Money Laundering Directive, which emphasizes continuous monitoring over periodic reviews.

Stablecoin integrations face similar scrutiny. Financial institutions processing digital asset payments must ensure that the underlying tokens comply with local regulatory status. AI-driven invoice auditing further strengthens this layer by detecting anomalies in billing data that may indicate fraud or non-compliance. These automated safeguards create a transparent audit trail, satisfying the stringent requirements of financial regulators in major jurisdictions.

-

Verify counterparty KYC status before initiation

-

Confirm stablecoin regulatory compliance in target jurisdiction

-

Audit AI-generated invoice data for anomalies

By embedding these checks into the rail, businesses eliminate the lag between detection and action. The result is a payment ecosystem where compliance is a feature of the infrastructure, not an afterthought. This shift is critical for maintaining trust and operational continuity in the evolving 2026 B2B landscape.

stablecoin invoicing legality

As of 2026, the legal standing of stablecoin invoices remains a fragmented landscape. While the European Union’s Markets in Crypto-Assets (MiCA) regulation provides a clear framework for stablecoin issuers, it does not automatically classify stablecoins as legal tender for debt settlement in all member states. In the United States, the lack of federal clarity means that enforceability depends on state-level commercial codes and specific contract terms. Global B2B agreements must explicitly define whether a stablecoin payment constitutes final discharge of debt or merely a conditional transfer.

Tax treatment for these transactions varies significantly by jurisdiction. In the EU, Value Added Tax (VAT) authorities generally view stablecoin transfers as equivalent to traditional currency exchanges, triggering tax events only upon conversion to fiat or acquisition of goods. The US Internal Revenue Service treats stablecoins as property, meaning each invoice payment may create a taxable capital gains or losses event if the stablecoin’s peg fluctuates. Companies must maintain rigorous transaction logs to reconcile these events for audit purposes.

No comments yet. Be the first to share your thoughts!