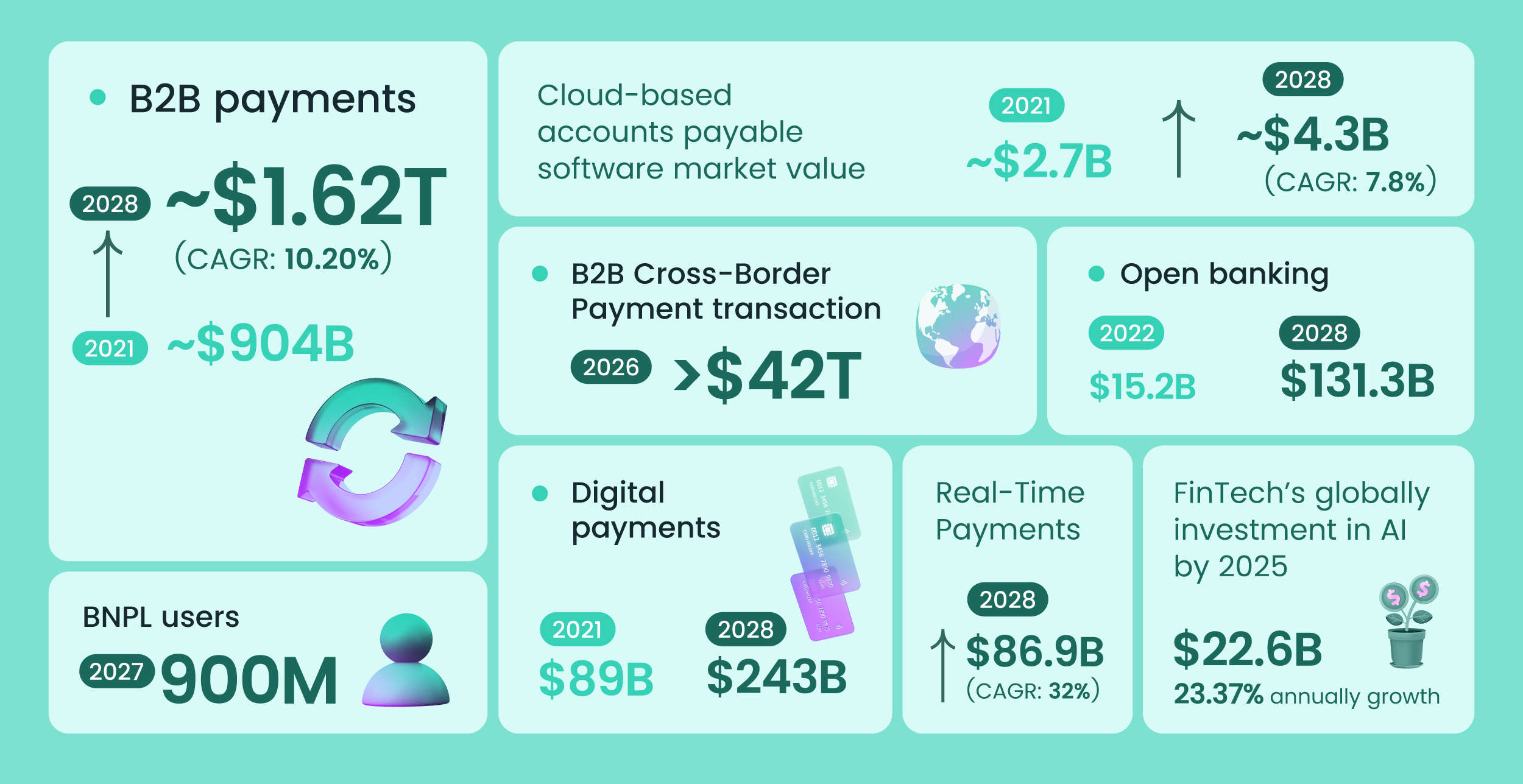

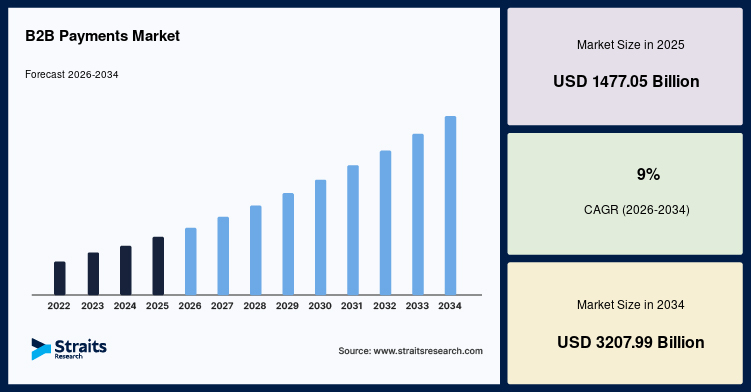

The scale of B2B payments and digital adoption

The global B2B payment landscape dwarfs consumer transactions. In 2026, total annual B2B payment volume is estimated between $150 trillion and $180 trillion USD. This figure represents over 85% of all global payment value, driven primarily by wholesale trade, supply chain logistics, and industrial procurement. For CFOs and treasury teams, this volume underscores that B2B payments are not merely a support function but the central nervous system of global commerce.

Despite this massive scale, the sector is undergoing a structural shift from legacy rails to digital infrastructure. Traditional methods, including paper checks and manual wire transfers, are being phased out in favor of automated, real-time platforms. The adoption of digital payment systems is accelerating, with enterprises increasingly prioritizing speed, transparency, and integration capabilities over simple transactional completion.

This transition is not uniform across all industries or regions. Large multinational corporations have largely migrated to integrated treasury management systems, while small and medium-sized enterprises (SMEs) are still bridging the gap. However, the pressure to modernize is universal, driven by the need for better cash flow visibility and reduced operational costs.

The move toward digital adoption is also reshaping vendor relationships. Suppliers are demanding faster payment terms, pushing buyers to adopt solutions that support dynamic discounting and early payment programs. This dynamic is forcing financial institutions and fintech providers to compete on integration depth and API reliability rather than just transaction fees.

How ai automation cuts days sales outstanding

AI is moving accounts receivable from a reactive administrative burden to a proactive cash flow engine. For B2B finance teams, the primary metric that matters is Days Sales Outstanding (DSO). By automating the entire invoice-to-cash cycle, artificial intelligence reduces the time between invoice delivery and cash receipt, directly improving liquidity without requiring additional working capital.

The most immediate impact comes from automated invoice processing. Traditional manual entry is slow and error-prone, leading to delays that push payment dates further out. AI systems use machine learning to extract data from diverse invoice formats, validate line items against purchase orders, and route approvals instantly. This eliminates the bottleneck of manual data entry, ensuring invoices are matched and approved in hours rather than days. According to industry analyses, this automation significantly reduces the administrative lag that typically inflates DSO in manufacturing and distribution sectors [1].

Beyond processing speed, AI-driven dispute resolution plays a critical role in shortening collection cycles. Disputes are the primary cause of delayed payments, often stalling cash flow for weeks while finance teams manually investigate discrepancies. AI tools can flag potential disputes before they arise by detecting anomalies in payment patterns or invoice data. When disputes do occur, AI can auto-generate responses or route them to the correct team member with all necessary context, reducing the resolution time from days to minutes. This proactive approach prevents small errors from becoming significant cash flow blockers [2].

The combination of faster processing and quicker dispute resolution creates a compounding effect on cash flow. As DSO decreases, companies free up capital that was previously tied up in unpaid invoices. This liquidity can be reinvested into growth initiatives or used to strengthen supplier relationships. For CFOs, the shift from manual AR management to AI automation is not just an efficiency upgrade; it is a strategic move to optimize working capital and reduce financial risk.

[1] 2026 B2B Payment Trends for Manufacturers and Distributors, OroInc [2] What's Changing in B2B Payments for 2026, TreviPay

stablecoin rails for cross-border settlement

The adoption of stablecoins for B2B invoicing and escrow is shifting from experimental pilot programs to core treasury infrastructure. By leveraging blockchain rails, enterprises can bypass the legacy correspondent banking network, drastically reducing both settlement times and foreign exchange friction. This transition addresses the persistent inefficiencies in cross-border trade, where traditional methods often tie up capital for days due to intermediary delays and opaque fee structures.

comparing settlement mechanics

The operational difference between traditional SWIFT transfers and stablecoin settlement is defined by speed and cost predictability. While SWIFT relies on a chain of correspondent banks that each take a cut and add latency, stablecoin transactions settle on-chain, often within minutes, regardless of the distance between parties. This structural advantage allows CFOs to optimize working capital by reducing the float period, turning days of idle liquidity into immediate available balance.

| Feature | Traditional SWIFT | Stablecoin Rail |

|---|---|---|

| Settlement Time | T+1 to T+3 | Minutes |

| FX Transparency | Opaque intermediary fees | Real-time mid-market rate |

| Availability | Business hours only | 24/7/365 |

| Cost Structure | High fixed + variable fees | Low network gas fees |

reducing fx fees through direct conversion

Stablecoin invoicing enables direct currency conversion at the point of payment, eliminating the need for multiple intermediaries to hold and convert funds. This direct path reduces the spread charged by correspondent banks and removes the hidden costs associated with traditional foreign exchange hedging for immediate settlements. For high-volume cross-border traders, this efficiency translates into significant margin preservation, particularly in volatile currency environments where traditional hedging instruments may be costly or slow to execute.

escrow and automated reconciliation

Beyond simple transfers, stablecoin smart contracts facilitate automated escrow services for complex B2B trade deals. Funds can be locked in a contract and released automatically upon fulfillment of predefined conditions, such as the delivery of goods or verification of services. This automation reduces the administrative burden of manual reconciliation and minimizes the risk of fraud or non-payment, providing a trustless environment for international partners who may lack established credit relationships.

Net terms versus virtual card adoption

The tension between traditional Net30/Net60 terms and virtual card adoption represents a fundamental shift in working capital management. For many CFOs, the choice is no longer just about cash flow timing, but about optimizing the cost of capital against operational friction.

Net terms remain the dominant infrastructure for B2B transactions, facilitating an estimated $150T–$180T in annual global payment volume. These terms allow buyers to preserve liquidity while suppliers manage credit risk. However, the hidden costs of extended payment periods—such as the cost of factoring or the administrative burden of managing receivables—can erode margins. Suppliers often offer early payment discounts to accelerate cash flow, but these discounts are frequently lost due to manual processing errors or lack of visibility.

Virtual cards address this gap by digitizing the discount capture process. By converting invoice payments into one-time-use virtual card transactions, buyers can secure early payment discounts (typically 1-3%) with minimal friction. This approach transforms a static liability into an immediate yield opportunity. The adoption curve is steep because virtual cards integrate with existing AP systems, requiring no change in supplier banking relationships. Yet, the transition is not seamless. Suppliers must be willing to accept card payments, and buyers must manage the interchange fees that accompany card transactions. The net benefit depends on whether the early payment discount exceeds the card processing fee—a calculation that varies by industry and supplier.

The competitive dynamic favors virtual cards in scenarios where the discount rate is high and the supplier base is receptive. For low-margin industries, the interchange fee can negate the discount, making Net terms more attractive. However, as real-time settlement infrastructure matures, the efficiency gains of virtual cards are likely to outweigh the fee costs, particularly for large-volume transactions.

implementation checklist for finance teams

Adopting AI-driven automation and real-time settlement rails requires a structured integration plan to manage risk and compliance. Finance leaders must evaluate their current tech stack against emerging standards for digital payments, ensuring that legacy systems can interface with modern APIs without creating data silos.

- Audit existing accounts receivable workflows to identify bottlenecks suitable for AI automation, such as invoice matching and dispute resolution.

- Select payment processors that support ISO 20022 messaging standards to facilitate smoother cross-border transactions and data richness.

- Establish a pilot program for stablecoin or real-time rail adoption, starting with a limited set of trusted suppliers to test settlement speed and volatility controls.

- Integrate comprehensive KYC/AML screening tools directly into the payment gateway to mitigate regulatory risks associated with new digital asset channels.

The transition from net-30 terms to instant settlement changes cash flow dynamics significantly. Teams should model the impact of reduced DSO (Days Sales Outstanding) on working capital requirements. This shift allows for more precise liquidity management but demands robust reconciliation processes to handle the increased volume of micro-transactions.

No comments yet. Be the first to share your thoughts!