Why 2026 Changes B2B Invoicing

2026 marks a definitive shift from optional automation to mandatory compliance for B2B invoicing. The regulatory landscape has tightened significantly, with major economies enforcing digital invoice standards that leave no room for manual workarounds. This is no longer a matter of efficiency; it is a requirement for doing business.

The European Union and Asia are leading this charge. France’s Finance Act, enacted in February 2026, mandates B2B e-invoicing for all businesses starting September 1, 2026. Similarly, India and Malaysia have implemented strict thresholds and timelines for digital validation. In India, businesses with an annual turnover exceeding Rs. 5 crore must comply from April 1, 2026, while Malaysia requires full validation through the MyInvois platform for companies earning over RM1 million annually.

Beyond regulation, the financial infrastructure is evolving. Stablecoin adoption is emerging as a practical solution for cross-border settlements, reducing the friction and cost associated with traditional wire transfers. As agentic AI begins to handle routine invoice processing, the focus for B2B companies must shift toward integrating these regulatory and technological changes immediately. The window for gradual adoption has closed.

5 B2B Invoicing Automation Trends for 2026

B2B invoicing automation in 2026 is defined by the convergence of AI-driven accuracy and emerging digital asset settlements. This roundup examines specific tools and regulatory shifts, including the integration of stablecoin payments, that are reshaping accounts receivable workflows.

-

AI-driven invoice data extraction accuracy

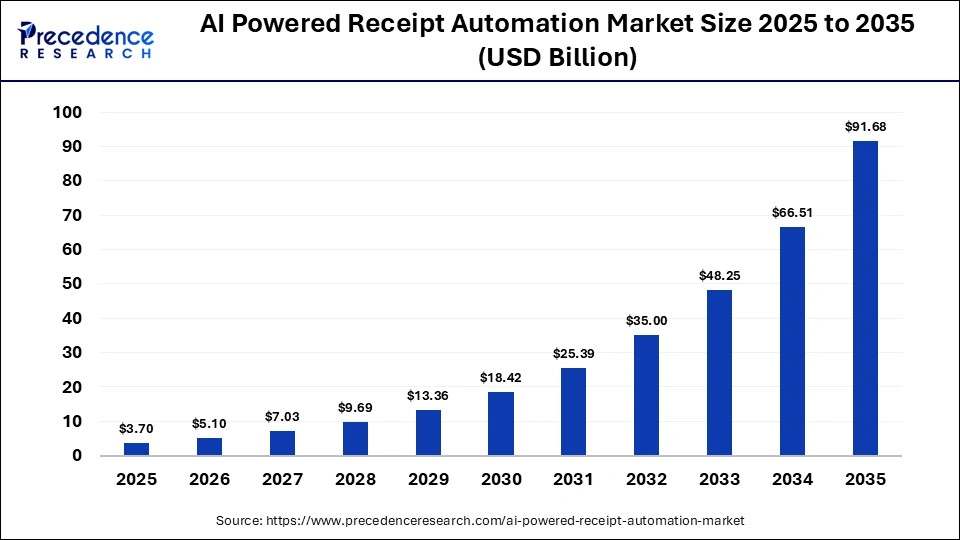

Modern AI models now achieve over 95% accuracy in extracting line-item data from complex B2B invoices, drastically reducing manual entry errors. Unlike older OCR systems, these tools understand context, handling varied formats without rigid templates. This precision allows finance teams to focus on exception handling rather than data validation. The market for AI-powered receipt automation is projected to reach significant heights, signaling a shift toward touchless processing as the new standard for operational efficiency. -

Real-time cross-border stablecoin settlements

Stablecoins are emerging as a critical infrastructure layer for cross-border B2B payments, offering near-instant settlement times compared to traditional SWIFT networks. By leveraging blockchain technology, companies can bypass intermediary banks, reducing fees and eliminating multi-day delays. This trend is particularly relevant for global supply chains where cash flow velocity directly impacts operational liquidity. As regulatory frameworks evolve, stablecoins provide a transparent, immutable record of transactions, enhancing trust between international trading partners. -

Embedded finance payment orchestration layers

Embedded finance platforms are integrating payment orchestration directly into procurement and ERP systems, creating seamless payment experiences without leaving the workflow. This approach allows businesses to dynamically select payment methods based on cost, speed, and regional availability. By abstracting the complexity of multiple payment gateways, companies can optimize transaction costs and improve approval rates. This structural shift is reshaping B2B fintech, enabling more flexible and efficient financial operations that adapt to real-time business needs. -

Automated regulatory compliance validation checks

Automated compliance tools are becoming essential for managing the growing complexity of global tax regulations and anti-money laundering (AML) requirements. These systems validate invoice data against changing legal standards in real-time, flagging discrepancies before payment execution. This proactive approach minimizes the risk of fines and reputational damage associated with non-compliance. By integrating compliance checks directly into the invoicing workflow, businesses ensure that every transaction adheres to local and international regulations, streamlining audit processes and enhancing financial governance. -

Predictive cash flow forecasting models

Advanced predictive analytics are transforming cash flow management by providing accurate forecasts based on historical data and real-time invoice status. These models identify potential cash shortfalls or surpluses weeks in advance, allowing finance teams to make informed decisions about investments and debt management. By leveraging machine learning, businesses can anticipate payment delays and adjust strategies accordingly. This proactive approach to cash flow visibility ensures liquidity stability and supports strategic growth initiatives without relying on guesswork or manual spreadsheets.

How stable invoice software works

Stablecoin invoicing software treats digital dollars as the settlement layer rather than just a messaging channel. When a buyer approves an invoice, the software triggers an instant transfer of a pegged asset like USDC or USDT. This bypasses the traditional correspondent banking network, which often adds days and hidden fees to cross-border payments. The speed comes from blockchain finality, meaning the seller sees confirmed funds in seconds, not weeks.

Cost reduction is the second major driver. Traditional international wire transfers can cost $20 to $50 per transaction, plus unfavorable foreign exchange spreads. Stablecoin transactions typically cost a fraction of that, often less than $1 regardless of the amount. For high-volume B2B suppliers, this margin difference compounds quickly. The software handles the conversion logic, ensuring the supplier receives the exact fiat value they invoiced, even if the buyer pays in a different currency.

Escrow capabilities add a layer of trust for new trading partners. Instead of sending payment upfront or waiting for net-30 terms, the buyer deposits the stablecoin into a smart contract escrow. The funds are released automatically once the supplier uploads proof of shipment or delivery. This mechanism reduces the risk of non-payment for sellers and overpayment for buyers, creating a neutral ground for international trade.

Top B2B payment automation providers

Selecting the right platform depends on your integration needs and scale. The following providers lead the market for B2B invoicing automation in 2026.

| Provider | Best For | Key Integration |

|---|---|---|

| LedgerUp | SaaS billing automation | ERP & Accounting |

| Stripe Billing | Developer-first payments | API & Webhooks |

| Chargebee | Subscription management | CRM & Billing |

| Maxio (Zuora) | Large enterprise scale | Salesforce |

For teams needing ready-to-deploy tools, these options cover core invoicing and payment workflows:

As an Amazon Associate, we may earn from qualifying purchases.

E-invoicing rules and thresholds for 2026

Regulatory timelines are shifting rapidly across major markets. In India, e-invoicing becomes mandatory from 1 April 2026 for businesses with an aggregate annual turnover exceeding Rs. 5 crore in the 2025-26 financial year. Companies with turnover above Rs. 10 crore must also adhere to a strict 30-day reporting window on the IRP portal starting that same date 1.

Malaysia is implementing a phased rollout through LHDN. Businesses earning between RM1 million and RM5 million annually must comply with the MyInvois validation platform from 1 January 2026. Full penalty enforcement for all eligible entities follows on 1 January 2027 2.

Europe continues to expand its mandate. France officially enacted its Finance Act on 2 February 2026, requiring all B2B transactions to be e-invoiced by 1 September 2026. These rules demand that all businesses, regardless of size, maintain the capability to issue and receive digital invoices directly.

No comments yet. Be the first to share your thoughts!